Nelson Capital Management

The yield curve has been a popular topic of discussion in the media in recent months. During the first week of December, many headlines declared that the yield curve had inverted. Inverted yield curves have generally been reliable indicators of past recessions, so this “inversion” gained a lot of attention. Does this mean we are headed for a recession? The short answer is that the media is focused on the wrong part of the curve and although the yield curve is flattening, we have not seen a true inversion yet. In normal economic periods, the yield curve slopes upward as longer bonds yield more than shorter bonds. Currently, short-term rates, which are controlled by the Federal Reserve, are rising faster than longer-term rates, creating a flat yield curve.

The yield curve has been a popular topic of discussion in the media in recent months. During the first week of December, many headlines declared that the yield curve had inverted. Inverted yield curves have generally been reliable indicators of past recessions, so this “inversion” gained a lot of attention. Does this mean we are headed for a recession? The short answer is that the media is focused on the wrong part of the curve and although the yield curve is flattening, we have not seen a true inversion yet. In normal economic periods, the yield curve slopes upward as longer bonds yield more than shorter bonds. Currently, short-term rates, which are controlled by the Federal Reserve, are rising faster than longer-term rates, creating a flat yield curve.

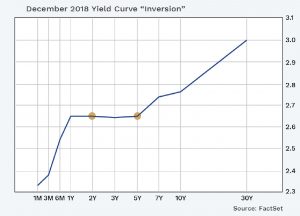

In early December, the yield on the 2-year Treasury was about 0.02% higher than the yield on the 5-year Treasury. The media highlighted this relationship as an inversion, but not only was the differential very small, it was likely a short-term trading aberration. The 2-year and 5-year also “inverted” in 1998, but this inversion was not followed by a recession. Generally, the relationship between the 2- and 10-year yields is a better indicator of a recession. At a spread of 0.18 percentage points, the 2-year and 10-year are close, but still in positive slope.

Historically, the probability of a recession doesn’t increase until the yield curve becomes substantially more inverted than a few basis points. The case for focusing on yield curves in the U.S. is based on the fact that they have made few false recession signals and many correct warnings. Still, it is unclear why the curve should matter, or which gap matters most.

Historically, the probability of a recession doesn’t increase until the yield curve becomes substantially more inverted than a few basis points. The case for focusing on yield curves in the U.S. is based on the fact that they have made few false recession signals and many correct warnings. Still, it is unclear why the curve should matter, or which gap matters most.

Individual investment positions detailed in this post should not be construed as a recommendation to purchase or sell the security. Past performance is not necessarily a guide to future performance. There are risks involved in investing, including possible loss of principal. This information is provided for informational purposes only and does not constitute a recommendation for any investment strategy, security or product described herein. Employees and/or owners of Nelson Roberts Investment Advisors, LLC may have a position securities mentioned in this post. Please contact us for a complete list of portfolio holdings. For additional information please contact us at 650-322-4000.

For the first time in a decade, short-term bond yields are increasing and offering meaningful income to buyers. When the Federal Reserve cut interest rates in 2007 and 2008 to help avert an economic collapse during the financial crisis, short-term bond yields dropped to near zero and have remained at 50-year lows. However, this trend appears to be changing.

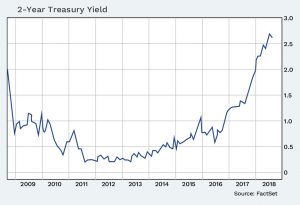

As signs of a tight job market and inflation pick up, the Federal Reserve has reversed course and increased its benchmark interest rate, while at the same time reducing the size of its balance sheet.  The Fed first bumped rates higher by 0.25% in December 2015. Since then, the Fed has increased rates by 0.25% seven times. The combination of these actions and the expectation of more rate hikes in the future has pushed the short end of the yield curve higher. The yield on the 2-year U.S. Treasury note crossed above 2.5% for the first time since March of 2008 and yields 2.77% today. This is a significant move—twelve months ago, the 2-year Treasury note was yielding 1.83%.

The Fed first bumped rates higher by 0.25% in December 2015. Since then, the Fed has increased rates by 0.25% seven times. The combination of these actions and the expectation of more rate hikes in the future has pushed the short end of the yield curve higher. The yield on the 2-year U.S. Treasury note crossed above 2.5% for the first time since March of 2008 and yields 2.77% today. This is a significant move—twelve months ago, the 2-year Treasury note was yielding 1.83%.

Flat Yield Curve

Short-term rates are rising faster than longer-term rates, flattening the yield curve. The gap between yields for short and long Treasuries narrowed to an 11-year low, a sign that the bond market is concerned about future economic growth. Longer bonds are influenced more by the expectations for growth and global demand and less by what the Fed does. The difference between the 2-year yield of 2.77% and the 10-year yielding 2.91% narrowed to 0.14%, its lowest point since August 2007.

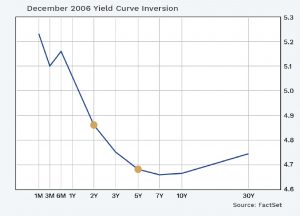

The relationship between short-term rates and long-term rates is important. If the differential goes negative, meaning the 10-year yield is below the 2-year yield, this is usually an indicator of a slowdown in economic growth. The yield curve has inverted ahead of each recession since 1975.

Outlook

In our view, the short end of the yield curve looks attractive and provides solid opportunities to earn income and stay defensive in a rising interest rate environment. We recommend keeping bond durations short and investing in high-quality bonds such as T-bills, CDs and short Treasury notes. These vehicles provide real returns, low volatility and ample liquidity.

Individual investment positions detailed in this post should not be construed as a recommendation to purchase or sell the security. Past performance is not necessarily a guide to future performance. There are risks involved in investing, including possible loss of principal. This information is provided for informational purposes only and does not constitute a recommendation for any investment strategy, security or product described herein. Employees and/or owners of Nelson Roberts Investment Advisors, LLC may have a position securities mentioned in this post. Please contact us for a complete list of portfolio holdings. For additional information please contact us at 650-322-4000.