Nelson Capital Management

Focus on the Data

Asset Management, Companies and Industries, Education, Investment Themes, Quarterly Commentary, The Economy

April 7, 2025

Focus on the Data

After two consecutive years of ~25% returns, the equity markets experienced a severe bout of volatility that left investors stunned. The S&P 500 fell 10% from its all-time high on February 19th, ending the quarter on March 31 down 4.3% year-to-date. The decline was initially triggered by the Trump administration’s tariff announcements in February, sending ripples through a market that had seemed unstoppable. But the real damage was done on April 3 and April 4, following the April 2 “Liberation Day” tariff announcements by the Trump administration. The S&P 500 fell over 10% in two days, suffering its worst two-day pullback since the depths of the pandemic in March 2020. By the end of Friday, April 4, the index was down over 17% from its mid-February high, while the NASDAQ moved into a bear market, having fallen over 21% from its high. As a group, the Magnificent 7 stocks finished the week down 28% from their mid-December all-time high.

After two consecutive years of ~25% returns, the equity markets experienced a severe bout of volatility that left investors stunned. The S&P 500 fell 10% from its all-time high on February 19th, ending the quarter on March 31 down 4.3% year-to-date. The decline was initially triggered by the Trump administration’s tariff announcements in February, sending ripples through a market that had seemed unstoppable. But the real damage was done on April 3 and April 4, following the April 2 “Liberation Day” tariff announcements by the Trump administration. The S&P 500 fell over 10% in two days, suffering its worst two-day pullback since the depths of the pandemic in March 2020. By the end of Friday, April 4, the index was down over 17% from its mid-February high, while the NASDAQ moved into a bear market, having fallen over 21% from its high. As a group, the Magnificent 7 stocks finished the week down 28% from their mid-December all-time high.

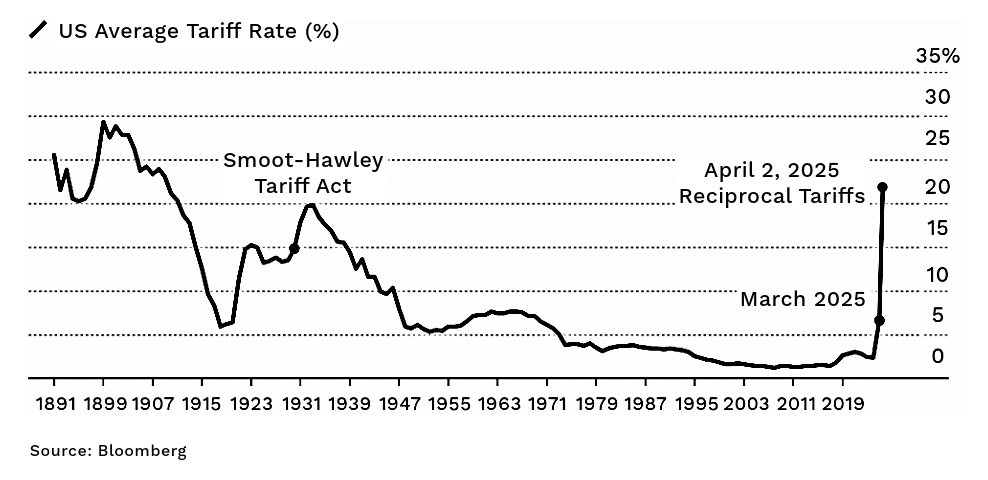

Before the tariff announcements, most investors had assumed Trump would use tariffs primarily as a negotiation tool, while closely watching the stock market, viewing it as a referendum on his presidency. This was the playbook during Trump’s first term. Many relied on the so-called “Trump put”—the belief that he would reverse course on any policy if markets reacted negatively. However, in Trump 2.0, this perceived safety net may not exist or may only activate at much lower levels. The proposed tariff rates far exceed those from his first administration, amplifying concerns about their scope and duration. In fact, the “Liberation Day” announcement brings the average tariff rate to the highest level in more than 100 years, representing a sharp lurch into aggressive protectionism. If the tariffs announced on April 2 stay as they are, the impact on global trade could be catastrophic. Adding to market unease, Trump has reiterated that he is not watching the stock market and has hinted at a “period of transition,” which many interpret as a likely recession. Trump does not care if there is pain—he claims it will be short-term, though we are not so sure.

With such dramatic market reactions, it is nearly impossible to ignore the headlines and the uncertainty they bring. Even so, we remain focused on the data. Since the Federal Reserve’s rate hike campaign began, we have tracked inflation and labor market indicators for signs of recession, renewed inflation, or a potential soft landing. Markets rallied in 2024 on the expectation of a soft landing, where inflation declines without triggering a recession or significant job losses, but the introduction of high tariffs has put this scenario at risk.

Markets rallied in 2024 on the expectation of a soft landing, where inflation declines without triggering a recession or significant job losses, but the introduction of high tariffs has put this scenario at risk.

The data reported so far still supports a soft landing. Headline inflation has fallen to 2.8%, while core inflation (excluding food and energy) stands at 3.1%. The Fed’s preferred measure, Core Personal Consumption Expenditures (PCE), has declined to 2.6%, approaching its stated 2% target. Following Trump’s election victory, concerns arose that inflation could reaccelerate due to policy priorities such as tighter immigration, deregulation, and tax cuts. Tariffs also represent an inflationary supply-side shock. Initially, Fed Chair Jerome Powell recently called tariff’s inflationary impact “transitory”—a surprising word choice given the Fed’s past missteps. But Powell’s more recent comments on April 4 noted that the announced tariffs were “significantly larger than expected,” meaning they could push inflation higher than previously thought. Tariffs can also dampen growth as businesses reduce hiring, spending, and investment, and so the announced tariff rates are also likely to have a more significant impact on growth. The Smoot-Hawley tariffs of the 1930s, which prolonged and possibly deepened the Great Depression, are a historical warning of protectionism’s economic risks.

Meanwhile, the labor market has not yet shown signs of slowing . Unemployment is at 4.2%, near historic lows, with 7.7 million job openings, still above pre-pandemic norms. A key recession indicator we monitor is the year-over-year change in nonfarm payrolls. Historically, when this measure falls below 1%, a recession follows soon after. Currently, it sits at 1.19%, suggesting a continued, albeit fragile, expansion.

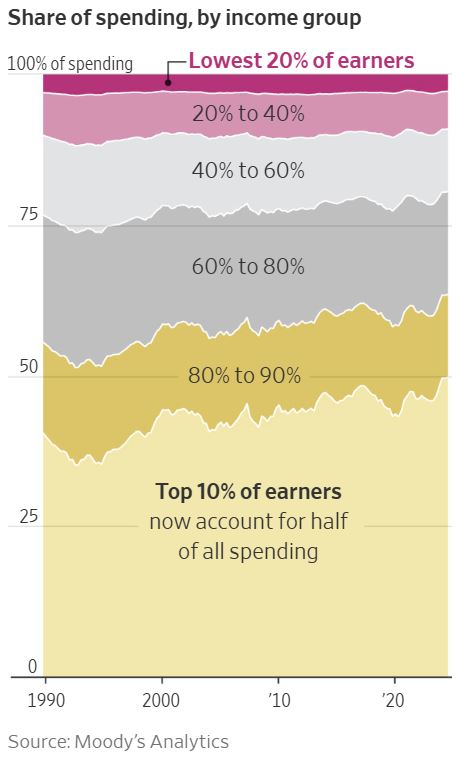

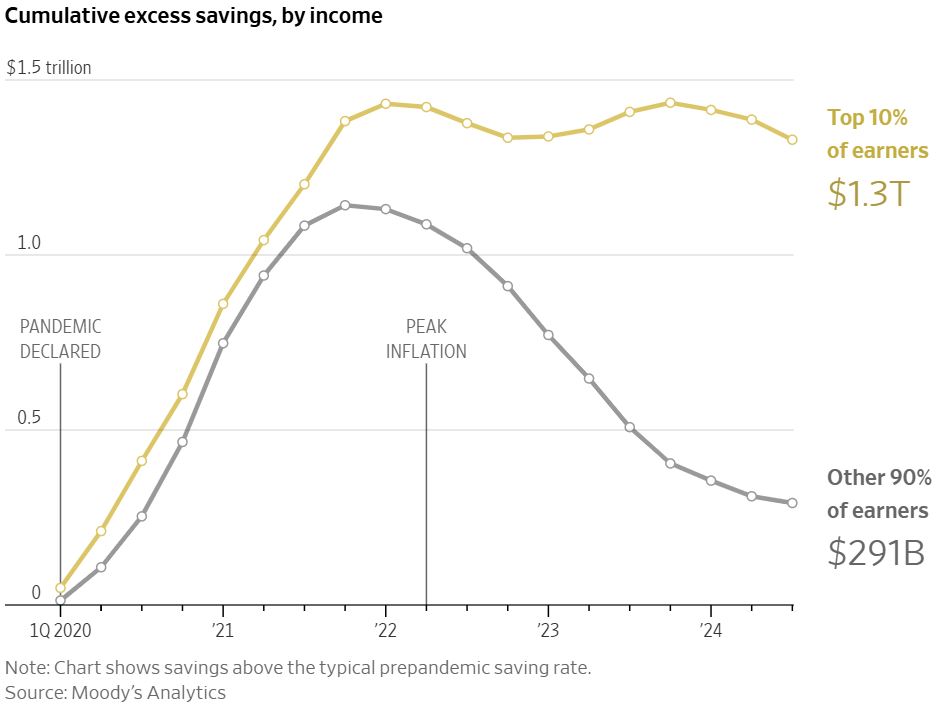

Consumer data is more mixed. Pandemic-era savings of lower-income consumers are nearly depleted, while top decile earners’ savings remain near 2022 highs. Mortgage delinquency rates are in line with historical averages, but auto and credit card delinquency rates are near 15-year highs. A recent Wall Street Journal article noted that the top 10% of earners now account for half of all spending. While this concentration is concerning, top earners could support economic growth, as long as their savings remain intact. A prolonged stock market downturn could threaten those savings.

The Fed has projected two rate cuts for the remainder of the year while maintaining a data-dependent stance. At its March meeting, the Fed held rates steady but announced plans to slow its balance sheet runoff beginning in April. Since the mid-2022 peak of $9 trillion, the balance sheet has been reduced to about $6.75 trillion with minimal disruption (2023 bank failures notwithstanding).

The likelihood of slower growth and higher prices from tariffs has reignited fears of stagflation, where growth stagnates and inflation soars. This scenario would leave the Fed in a difficult position: if inflation reaccelerates, the Fed should be hesitant to cut rates, but if growth stagnates, they should be eager to cut rates. On the positive side, Nelson Capital’s portfolios are performing better than the S&P 500 and the market pullback has alleviated some pressure from inflated equity valuations. International markets outshined US markets for the first time in years, and the safe-haven appeal of US Treasuries reaffirms the benefit of maintaining a diversified portfolio. The decline in the Magnificent 7 has also highlighted opportunities within undervalued sectors that offer more attractive valuations. We continue to closely monitor key data, particularly the nonfarm payroll growth, for early signs of an economic downturn.

Individual investment positions detailed in this post should not be construed as a recommendation to purchase or sell the security. Past performance is not necessarily a guide to future performance. There are risks involved in investing, including possible loss of principal. This information is provided for informational purposes only and does not constitute a recommendation for any investment strategy, security or product described herein. Employees and/or owners of Nelson Capital Management, LLC may have a position securities mentioned in this post. Please contact us for a complete list of portfolio holdings. For additional information please contact us at 650-322-4000.

Receive our next post in your inbox.