Nelson Capital Management

Reopening Drives Valuations Higher

April 9, 2021

Reopening Drives Valuations Higher

The lofty valuations we noted at the end of 2020 pushed even  higher through the first quarter of this year, rising above the dot-com era valuations of 1999. Pockets of frothiness are still evident in some places such as the cryptocurrency market, the IPO market, and in so-called “meme stocks” like GameStop, which gained attention at the end of January. But overall market valuations appear to be based on this year’s anticipated reopening of the economy, along with the expected pent-up demand from consumers later this year as the vaccine rollout gains steam. President Biden has asked states to make all adults eligible for vaccination by May 1. As of this writing, CDC data show more than 121 million doses have already been administered, and roughly one in six American adults has been fully vaccinated.

higher through the first quarter of this year, rising above the dot-com era valuations of 1999. Pockets of frothiness are still evident in some places such as the cryptocurrency market, the IPO market, and in so-called “meme stocks” like GameStop, which gained attention at the end of January. But overall market valuations appear to be based on this year’s anticipated reopening of the economy, along with the expected pent-up demand from consumers later this year as the vaccine rollout gains steam. President Biden has asked states to make all adults eligible for vaccination by May 1. As of this writing, CDC data show more than 121 million doses have already been administered, and roughly one in six American adults has been fully vaccinated.

Although the labor market has not yet recovered—the U.S. is still down almost 10 million jobs since the pandemic started—the expectation is that these jobs will return quickly upon reopening. The initial release of the first quarter Gross Domestic Product (GDP) data will occur on April 29 and is projected to be 4.7% quarter-over-quarter. Some economists are predicting that 2021 could usher in the highest U.S. GDP growth that we have seen since 1984.

Furthermore, the unprecedented fiscal and monetary stimulus that was injected into the system has increased U.S. money supply by 25%, the largest year-over-year growth on record. This begs the question: Will we see inflation rise? Although the latest Consumer Price Index (CPI) inflation data was underwhelming, we are seeing pressures build. Prices of raw materials (particularly lumber, steel, and copper) have risen substantially as

the pandemic drove an unexpected wave of demand. When the pandemic first hit, many alongside increased demand, particularly as most supply has not come back online, with many rigs remaining idle. On recent earnings calls, CFOs have discussed using price increases to pass higher input costs on to consumers. Moreover, we could see even more fiscal stimulus down the road. With its most recent $1.9 trillion coronavirus stimulus package passed, the Biden administration has turned its focus to infrastructure. Democrats passed the latest coronavirus stimulus through reconciliation, gaining no Republican support. Given the wide range of disagreement on size, scope, and funding source of a new infrastructure bill, it seems improbable that the two sides will reach a bipartisan agreement. The administration has mentioned possible corporate and wealthy individual tax increases, although it is difficult to imagine tax increases being passed while the economy is still recovering. Democrats also still need to contend with a razor-thin majority in Congress and some moderate-leaning members of the party.

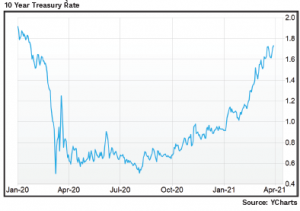

Meanwhile, the yield on the 10-year U.S. Treasury has increased swiftly, from 0.93% at the beginning of the year to 1.75%. Some have pointed to this as a sign of elevated inflation expectations, while others have said this reflects growing confidence in the U.S. economic outlook, but the Federal Reserve has downplayed concerns, indicating that it does not plan to hike interest rates or ease its bond-buying program any time soon. In any case, increasing yields have shuffled the equity market and created new leaders. Growth and momentum stocks, such as Apple (tkr: AAPL), Netflix (tkr: NFLX), and Amazon (tkr: AMZN) which have outperformed dramatically over the past decade, have lagged so far in 2021. The best performing sectors year-to-date are financials and energy stocks, both considered value sectors that have trailed the broader market over the past several years and performed particularly poorly in 2020.

Meanwhile, the yield on the 10-year U.S. Treasury has increased swiftly, from 0.93% at the beginning of the year to 1.75%. Some have pointed to this as a sign of elevated inflation expectations, while others have said this reflects growing confidence in the U.S. economic outlook, but the Federal Reserve has downplayed concerns, indicating that it does not plan to hike interest rates or ease its bond-buying program any time soon. In any case, increasing yields have shuffled the equity market and created new leaders. Growth and momentum stocks, such as Apple (tkr: AAPL), Netflix (tkr: NFLX), and Amazon (tkr: AMZN) which have outperformed dramatically over the past decade, have lagged so far in 2021. The best performing sectors year-to-date are financials and energy stocks, both considered value sectors that have trailed the broader market over the past several years and performed particularly poorly in 2020.

Looking ahead, we are evaluating our portfolio exposure across several themes: international (developed and emerging) vs. domestic, growth vs. value, large-cap vs. small-cap. The recent reshuffling of market leaders reminds us of the importance of having a diversified strategy and balanced exposure to a variety of sectors, regions, and styles. We think inflation fears will play a major role, even if we do not see actual inflation in the near term. We remain skeptical of growth and momentum valuations, which could be further challenged if rates really take off.

Individual investment positions detailed in this post should not be construed as a recommendation to purchase or sell the security. Past performance is not necessarily a guide to future performance. There are risks involved in investing, including possible loss of principal. This information is provided for informational purposes only and does not constitute a recommendation for any investment strategy, security or product described herein. Employees and/or owners of Nelson Capital Management, LLC may have a position securities mentioned in this post. Please contact us for a complete list of portfolio holdings. For additional information please contact us at 650-322-4000.

Receive our next post in your inbox.