Nelson Capital Management

A Return to Volatility

Asset Management, Investment Themes, The Economy

April 12, 2018

Economic Overview

2018 began with the U.S. markets posting a record 15th consecutive month of positive returns. The Dow Jones Industrial Average rose above 26,600, its highest level ever, by the end of January. Since then, investors have been on a roller coaster ride. From the high, the Dow Jones declined 10%, falling 2,756 points, bounced back 7.7% to 25,700, before ending the quarter at 24,103. For the entire quarter, the Dow Jones fell 1.96% and the S&P 500 fell 0.76%

The last ten weeks of the first quarter were not for the faint of heart. This volatility feels especially painful following a prolonged period of unusually quiet and steadily rising stock markets. In spite of the market gyrations, there are plenty of signs that this bull market is not over. Projections for U.S. GDP growth were recently revised upward to 2.7%. Global growth estimates are equally optimistic, driven by improved confidence, increased investment and robust global trade. Unemployment remains low at 4.1%. Wages rose 2.9% in January, the biggest year-over-year gain since 2009. U.S. corporations are expected to benefit from the significant tax cut that took effect in 2018, with analysts estimating that corporate earnings will grow over 18.5% this year. Companies are returning their improved earnings to shareholders through share buybacks and higher dividend payments. Inflation has climbed toward the Federal Reserve’s stated 2% goal. In March, the Fed hiked its benchmark Federal Funds Target Rate by a quarter of a percentage point to 1.5-1.75%, maintaining its path of raising interest rates alongside a rosy growth forecast.

The last ten weeks of the first quarter were not for the faint of heart. This volatility feels especially painful following a prolonged period of unusually quiet and steadily rising stock markets. In spite of the market gyrations, there are plenty of signs that this bull market is not over. Projections for U.S. GDP growth were recently revised upward to 2.7%. Global growth estimates are equally optimistic, driven by improved confidence, increased investment and robust global trade. Unemployment remains low at 4.1%. Wages rose 2.9% in January, the biggest year-over-year gain since 2009. U.S. corporations are expected to benefit from the significant tax cut that took effect in 2018, with analysts estimating that corporate earnings will grow over 18.5% this year. Companies are returning their improved earnings to shareholders through share buybacks and higher dividend payments. Inflation has climbed toward the Federal Reserve’s stated 2% goal. In March, the Fed hiked its benchmark Federal Funds Target Rate by a quarter of a percentage point to 1.5-1.75%, maintaining its path of raising interest rates alongside a rosy growth forecast.

So what caused the volatility? The first jolt came during the first week of February, after the better than- expected wage growth number sparked concerns that inflation might be getting out of hand, which could cause the Fed to increase rates at a more rapid pace. Furthermore, Congress passed a two-year spending deal, increasing defense and other forms of discretionary spending. Coupled with the tax cut, the government is anticipated to add over $1 trillion to the deficit in the coming fiscal year, adding more fuel to the U.S. economic engine.

The second bout of volatility came a few weeks later alongside headlines detailing a brewing trade scuffle with China. In March, President Trump announced trade measures including tariffs on various goods imported from China. These tariffs will target up to $60 billion of annual imports to the U.S. from China, centered largely on the steel industry. China, in turn, responded by imposing tariffs on about $3 billion worth of U.S. imports.

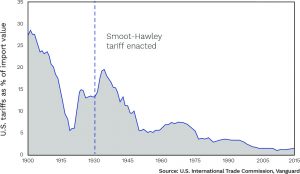

The markets, fearing that this trade scuffle could escalate into a trade war, fell over 1,000 points over two trading sessions. The trading relationship between the U.S. and China is important for both countries, and disrupting it could have lasting ripple effects through the global economy. However, the U.S. remains the most open market, and we do not see that position changing anytime soon. U.S. tariffs as a percentage of import value have been falling since the 1930s and have been below 5% for more than four decades. The Trump administration enacted tariffs on steel and aluminum—products that together represent less than 2% of total imports to the U.S. Furthermore, with several countries now exempted from these tariffs, the actual number of imports affected is even lower. At this point, we believe that talk of a “trade war” is, in fact, simply posturing by the Trump administration to negotiate better trading terms with China.

The markets, fearing that this trade scuffle could escalate into a trade war, fell over 1,000 points over two trading sessions. The trading relationship between the U.S. and China is important for both countries, and disrupting it could have lasting ripple effects through the global economy. However, the U.S. remains the most open market, and we do not see that position changing anytime soon. U.S. tariffs as a percentage of import value have been falling since the 1930s and have been below 5% for more than four decades. The Trump administration enacted tariffs on steel and aluminum—products that together represent less than 2% of total imports to the U.S. Furthermore, with several countries now exempted from these tariffs, the actual number of imports affected is even lower. At this point, we believe that talk of a “trade war” is, in fact, simply posturing by the Trump administration to negotiate better trading terms with China.

Alongside this tariff news, we saw distressing headlines over possible geopolitical instability with the appointment of John Bolton as National Security Advisor. Bolton is known for his very hawkish views, and his appointment, combined with that of Mike Pompeo as CIA director, caused many to speculate that the president is building a “war cabinet.” However, we currently have no reason to suspect there is cause for imminent concern.

Fifteen months of positive performance with little volatility had escalated valuations to the brink of euphoria. However, this recent downturn brought market P/Es to more reasonable levels. Market volatility has clearly returned, and it seems particularly uncomfortable after such a prolonged period without it. Markets tend to fear uncertainty, and even though underlying fundamentals are healthy, there are plenty of unknowns. Heightening trade conflict with China could escalate to a trade war. The carousel of presidential advisors could lead to geopolitical instability. The Fed could increase interest rates too rapidly, disrupting economic growth and leading to a recession. At this point, none of these pressures are significant enough to derail the current global economic expansion, but each is worthy of our attention. In any case, the volatility in the markets is likely to persist as long as the headlines continue to focus on these unknowns.

We maintain our assertion that the next recession will ultimately be caused by the Fed overtightening, but this is not something we anticipate happening in the near term. In the meantime, rates are going to chase inflation up, and until inflation peaks, bonds will not have much of a real return. For now, the continued volatility in the market allows active managers like us to identify opportunities to enter the market at more attractive valuations.

Individual investment positions detailed in this post should not be construed as a recommendation to purchase or sell the security. Past performance is not necessarily a guide to future performance. There are risks involved in investing, including possible loss of principal. This information is provided for informational purposes only and does not constitute a recommendation for any investment strategy, security or product described herein. Employees and/or owners of Nelson Roberts Investment Advisors, LLC may have a position securities mentioned in this post. Please contact us for a complete list of portfolio holdings. For additional information please contact us at 650-322-4000.

Receive our next post in your inbox.