Nelson Capital Management

Exuberance Extended

Asset Management, Companies and Industries, Education, Fixed Income, Investment Themes, Quarterly Commentary, The Economy

January 6, 2025

Exuberance Extended

2024 marked another great year for the equity markets. The S&P 500 rose 25%, following the 26% increase in 2023. The last time the benchmark index saw two consecutive 20%+ years was in 1998. Gold had its best year since 2010, and the price of Bitcoin doubled. The strong equity market returns were driven by a handful of large companies. If 2023 was the year of the “Magnificent 7” (Amazon, Apple, Alphabet, Meta, Microsoft, NVIDIA, and Tesla), 2024 might be considered the year of the “BATMMAAN” (Broadcom, Apple, Tesla, Microsoft, Meta, Amazon, Alphabet, NVIDIA), as Broadcom’s latest earnings announcement propelled it into the spotlight as the newest AI darling. These eight companies accounted for over half of the S&P 500’s return. Excluding these companies, the remainder of the index returned about 10% for the year.

2024 marked another great year for the equity markets. The S&P 500 rose 25%, following the 26% increase in 2023. The last time the benchmark index saw two consecutive 20%+ years was in 1998. Gold had its best year since 2010, and the price of Bitcoin doubled. The strong equity market returns were driven by a handful of large companies. If 2023 was the year of the “Magnificent 7” (Amazon, Apple, Alphabet, Meta, Microsoft, NVIDIA, and Tesla), 2024 might be considered the year of the “BATMMAAN” (Broadcom, Apple, Tesla, Microsoft, Meta, Amazon, Alphabet, NVIDIA), as Broadcom’s latest earnings announcement propelled it into the spotlight as the newest AI darling. These eight companies accounted for over half of the S&P 500’s return. Excluding these companies, the remainder of the index returned about 10% for the year.

We have entered a new era of optimism. The forward price-to-earnings ratio of the S&P 500 is now over 22x, matching the high in late 2021 and closing in on the 1999 dot-com bubble peak of 24x.

We have entered a new era of optimism. The forward price-to-earnings ratio of the S&P 500 is now over 22x, matching the high in late 2021 and closing in on the 1999 dot-com bubble peak of 24x. There are reasons to believe that these valuations might be justified: Inflation has generally trended lower, inching closer to the Federal Reserve’s 2% target, while the labor market remains remarkably resilient, indicating that the US economy may achieve the elusive “soft landing.” Jaw-dropping advancements in AI have promised to usher in an era of skyrocketing productivity that will supercharge growth over the next decade. The equity markets also saw a post-election surge, driven by hopes that the second Trump Administration will foster growth driven by lower taxes and deregulation. Together, these dynamics have produced a dizzying cocktail of exuberance.

Former Federal Reserve Board Chairman Alan Greenspan famously popularized the term “irrational exuberance” to warn that asset prices might be reaching unsustainable levels and that the stock market might be overvalued. Many remember Greenspan as prescient since these words were uttered before the dot-com bubble burst in 2000. But what some people forget is that this now-famous speech was given on December 5, 1996, a full three years before the actual collapse. This serves as a reminder to us that markets may indeed be overvalued, but that the overvaluation could continue for quite some time. Trying to time the market is a fool’s errand.

Instead, we continue to stay invested and monitor the most probable underlying risks, namely that inflation could reignite. Inflation has approached the Fed’s 2% target, but it seems stuck in neutral around 2.5-3%, as the “last mile” is proving challenging to bring down. The shelter component, which accounts for about one third of the calculation, remains stubbornly high, along with prices for most services. The incoming Trump administration has pitched growth-friendly policies like lower taxes and deregulation, but we observe that these could also spur inflation higher. Trump’s other two policy priorities, higher tariffs and immigration curbs, are also generally inflationary. We also observe the surging power demand from AI. Data centers require a massive amount of electricity to train and operate complex AI models. This is likely to lead to higher electricity bills for consumers, which would also be inflationary.

The Fed began its easing cycle in 2024, cutting its target benchmark rate by 0.50% in September and finishing the year with two 0.25% cuts each in November and December. But on December 18 alongside the 0.25% interest rate cut announcement, Fed Chairman Jerome Powell outlined the Fed’s plan to cut rates by only half a percent in 2025, rather than the full percent cut the Fed had outlined at its prior meeting. The stock market threw a temper tantrum following the announcement, and the S&P 500 index had fallen about 3% by the day’s end. Looking ahead, if inflation reverses course and begins to reaccelerate, we anticipate that the Fed will either need to pull back on its plan to cut rates or—God forbid—hike interest rates. We suspect that this would lead to an even bigger temper tantrum, perhaps on par with the bear market experienced in 2022 in response to the Fed’s aggressive interest rate hikes.

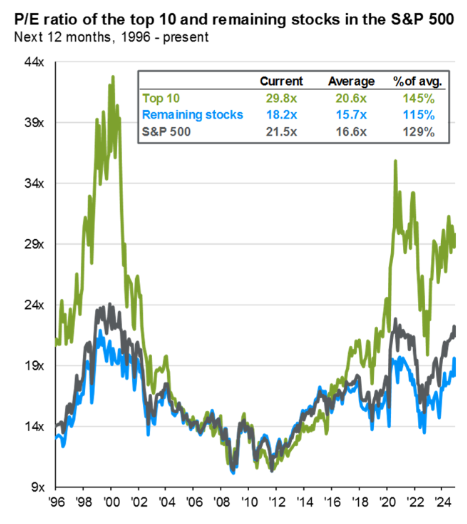

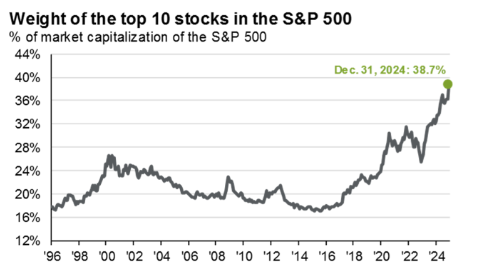

The other risk to the status quo might be a sentiment shift, which is hard to predict, but still worth discussing. The S&P 500 has never been so concentrated. The top ten stocks in the index now make up 38.7% of the index. The combined market capitalization of the Magnificent 7 companies is larger than the combined market cap of all major European stock exchanges. These seven behemoths are at the epicenter of a tectonic shift in technology driven by AI developments. They also maintain fortress balance sheets and churn out large amounts of cash from their core businesses. It is hard to imagine what could cause these stocks to fall out of favor. Valuation could be the only risk, as these stocks are expensive. The aggregate forward P/E ratio of the top 10 stocks in the index is just under 30x, compared to a 30-year average level of 20.6x. A reckoning on these stretched valuations could cause P/E multiple compression in this group and might even push investors to look at some unloved areas of the market, such as small-cap, international, or more traditional value stocks.

Individual investment positions detailed in this post should not be construed as a recommendation to purchase or sell the security. Past performance is not necessarily a guide to future performance. There are risks involved in investing, including possible loss of principal. This information is provided for informational purposes only and does not constitute a recommendation for any investment strategy, security or product described herein. Employees and/or owners of Nelson Capital Management, LLC may have a position securities mentioned in this post. Please contact us for a complete list of portfolio holdings. For additional information please contact us at 650-322-4000.

Receive our next post in your inbox.