Nelson Capital Management

Hazards Exist that are not Marked

Asset Management, Companies and Industries, Education, Investment Themes, Quarterly Commentary, The Economy

October 2, 2024

Hazards Exist that are not Marked

Markets continued their winning streak throughout the third quarter, with the S&P 500 gaining 5.9%, bringing its year-to-date return to 22.1%. The optimism that the US economy will coast into a soft landing grew, supported by three consecutive reports showing that inflation came in lower than most economists expected. The labor market continued to soften, yet unemployment remains low, hovering just over 4%. Equity market returns were also boosted by strong earnings growth, with S&P 500 companies on track to grow earnings per share by 10% for 2024. Analysts are even more optimistic about 2025, projecting 15% earnings growth for next year, helped by heavy investment in new artificial intelligence developments and applications.

Markets continued their winning streak throughout the third quarter, with the S&P 500 gaining 5.9%, bringing its year-to-date return to 22.1%. The optimism that the US economy will coast into a soft landing grew, supported by three consecutive reports showing that inflation came in lower than most economists expected. The labor market continued to soften, yet unemployment remains low, hovering just over 4%. Equity market returns were also boosted by strong earnings growth, with S&P 500 companies on track to grow earnings per share by 10% for 2024. Analysts are even more optimistic about 2025, projecting 15% earnings growth for next year, helped by heavy investment in new artificial intelligence developments and applications.

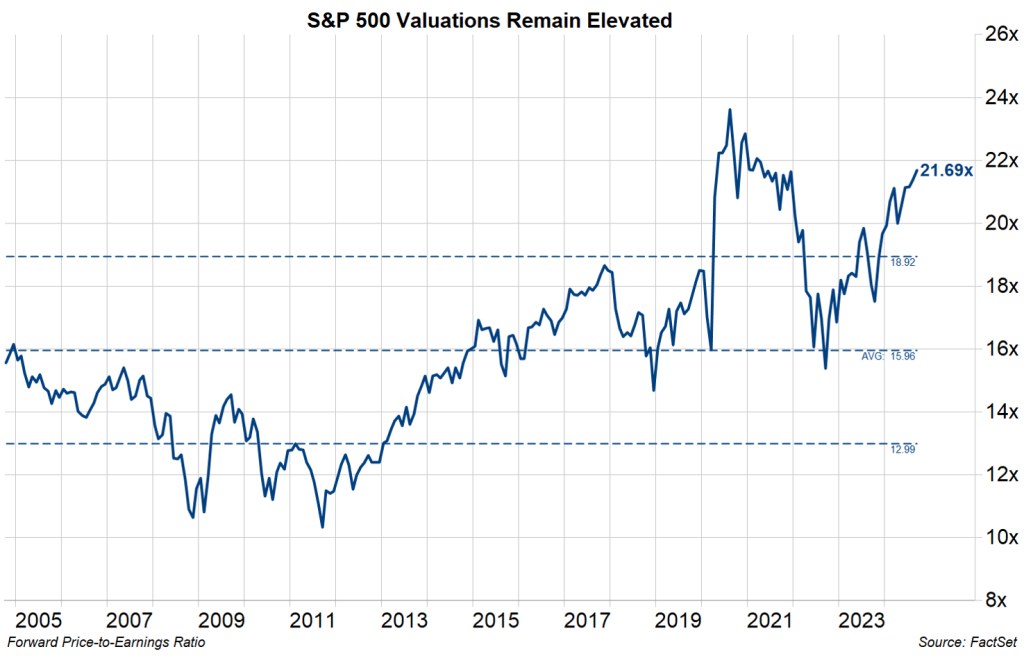

Valuations, as measured by the price of the S&P 500 relative to the forward-looking (and very rosy) analyst earnings estimates, are currently at 21.7x. This is just below the recent peak of 22x of 2021 and much higher than the 30-year average of 16.9x. Market participants have largely bought into the soft-landing narrative, and few skeptics remain.

As stewards of client assets, we feel it is our responsibility to maintain some degree of skepticism, especially when the consensus view is idealistic. Heading into the fall, we are a few short months away from ski season. At many ski mountains, signage warns skiers: “HAZARDS EXIST THAT ARE NOT MARKED.” We retain a degree of caution and look for the hazards buried underneath the fresh powder.

The yield curve has long been considered a recession indicator. Traditionally, when the yield curve “inverts” and short-term yields are higher than long-term yields, this has been followed by a recession, usually after the curve returns to normal. The spread between the 2-year Treasury and the 10-year Treasury is the most popular metric. After the longest inversion on record, the 2-10 spread is now positive (no longer inverted). History tells us that a recession is coming.

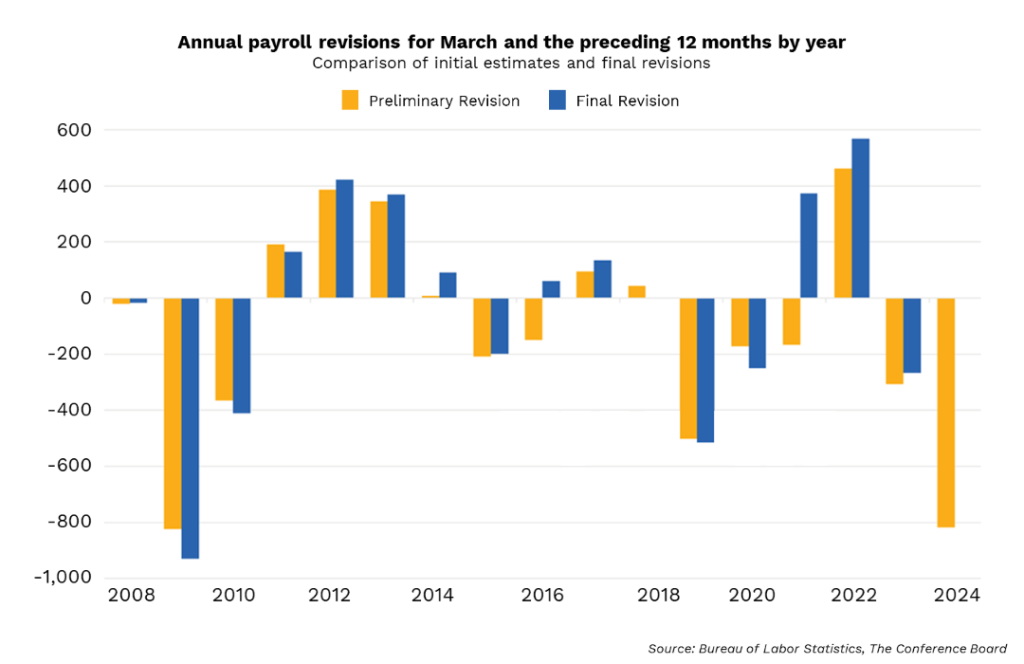

Although the labor market can generally be currently characterized as resilient, there are cracks worth noting. The Bureau of Labor Statistics (BLS) periodically revises its estimates of job creation data. The first revision was released in August, with the BLS indicating that total nonfarm employment for the year ending March 2024 was 818,000 lower than previously reported. This was the largest negative revision to the data since March of 2009—the apex of the financial crisis. The July labor report also triggered the Sahm Rule, a recession indicator coined by economist Claudia Sahm, which tracks the three-month moving average of the unemployment rate. When this measure increases by 0.5% or more above the 12-month low, the Sahm Rule flashes its recession indicator. Arguing that the US will avoid a recession now requires some version of the argument that “it’s different this time.”

Consumer data has been mixed. While the high-income consumer is in good shape, consumers with lower incomes are struggling. We have noted for several months the rising delinquencies for auto and credit card loans as lower-income consumers struggle under the weight of crushing inflation and very high interest rates for these loans. Dollar Tree (tkr: DLTR) and Dollar General (tkr: DG) fell 22% and 32% respectively at their latest earnings announcements. Both indicated that their core consumer is financially constrained, and spending remains weak. On the other hand, high-income consumers are in better shape, boosted by rising brokerage account balances and higher home values.

While we would love to believe the current consensus view that the US will avoid a recession completely and glide gracefully into a soft landing, turbocharged by an AI-driven earnings growth cycle, we remain focused on uncovering the hazards that may derail this scenario.

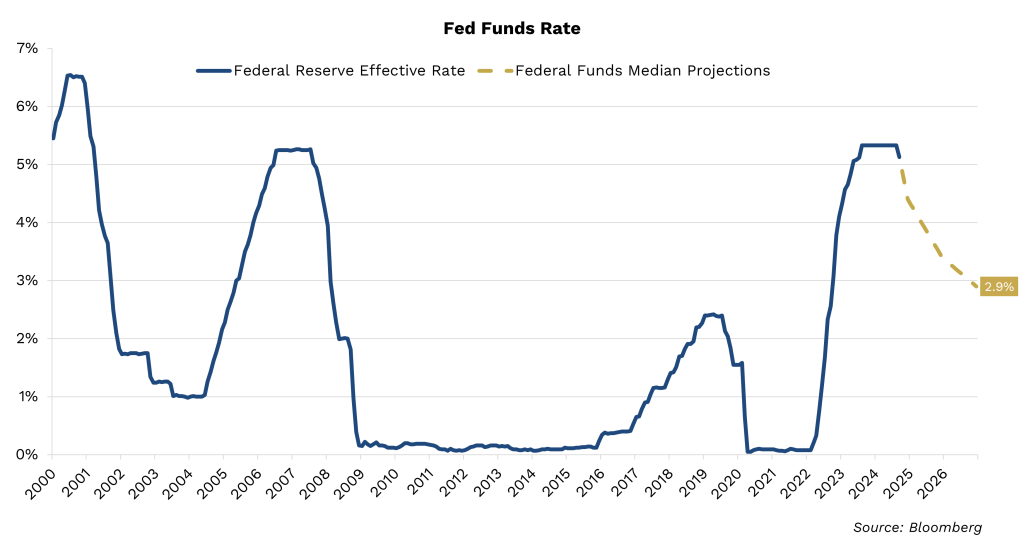

The Federal Reserve has taken note of the weakening labor market and has refocused its mandate from reducing inflation to stabilizing the economy. The Fed began its interest rate reduction cycle with a 0.5% cut, while telegraphing another 0.5% cut to its benchmark rate between now and the end of the year. The markets are predicting an even larger 0.75% cut by the end of 2024, with another full percentage point cut priced in by this time next year. It is difficult to reconcile a scenario where the Fed slashes rates by 2.5% over a 12-month period without an economic recession.

While we would love to believe the current consensus view that the US will avoid a recession completely and glide gracefully into a soft landing, turbocharged by an AI-driven earnings growth cycle, we remain focused on uncovering the hazards that may derail this scenario. Labor markets can turn very quickly, and so we track the year-over-year change in the nonfarm payroll data closely, as we believe a dip below 1% growth can indicate a downshift in hiring and an impending recession. We are also watching consumer data for signs of instability spreading beyond the lower-income cohort. Meanwhile, we are monitoring the intensifying geopolitical conflicts in the Middle East, Ukraine as well as the Taiwan-China tensions. If these conflicts morph into a new world war, this would likely lead to increased volatility, disruption of supply chains, and a spike in commodity prices. While we do not see impending signs of inflation reigniting, this is the other possibility we are examining, particularly with presidential campaign promises of increased spending and higher tariffs, both of which could fan the flames of inflation and force the Fed to reverse course.

Individual investment positions detailed in this post should not be construed as a recommendation to purchase or sell the security. Past performance is not necessarily a guide to future performance. There are risks involved in investing, including possible loss of principal. This information is provided for informational purposes only and does not constitute a recommendation for any investment strategy, security or product described herein. Employees and/or owners of Nelson Capital Management, LLC may have a position securities mentioned in this post. Please contact us for a complete list of portfolio holdings. For additional information please contact us at 650-322-4000.

Receive our next post in your inbox.