Nelson Capital Management

What is Financial Planning?

September 18, 2023

What is Financial Planning?

Planning is essential to any successful outcome and personal finance is no different. But what is a financial plan and how can you make one?

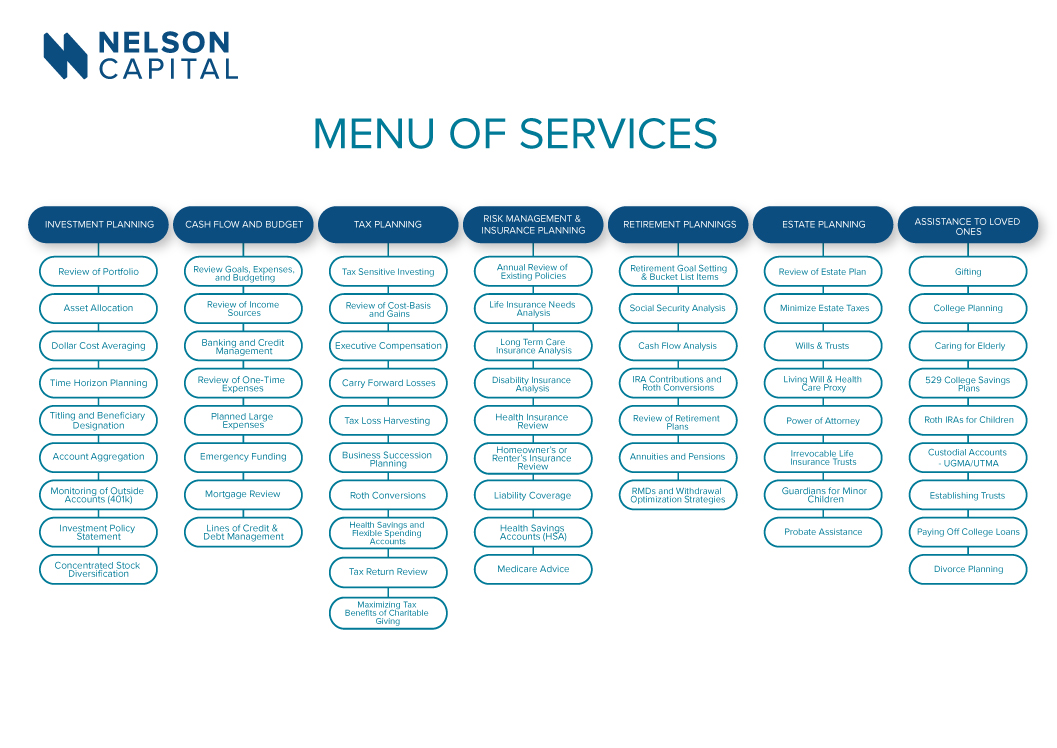

Financial planning is the process of comprehensively reviewing your current financial situation and creating a plan to achieve your desired goals. It encompasses investment planning, cash flow and budgeting, tax planning, risk management and insurance planning, retirement planning, estate planning, and assisting loved ones.

Financial planning is the process of comprehensively reviewing your current financial situation and creating a plan to achieve your desired goals. It encompasses investment planning, cash flow and budgeting, tax planning, risk management and insurance planning, retirement planning, estate planning, and assisting loved ones.

Investment planning involves reviewing your portfolio of investments. This includes analyzing asset allocation: how assets are invested across various classes such as stocks, bonds, and cash. The asset allocation will determine the risk/return profile of your portfolio. Asset allocation may be different depending on the account type and time horizon to utilizing the funds. The allocation and target return you and your financial advisor agree upon should be in line with your risk tolerance and should be memorialized in an Investment Policy Statement (IPS). Some financial advisors can assist with monitoring outside accounts (e.g., your 401k), or some may offer more in-depth strategies such as concentrated stock diversification.

Cash flow and budgeting is the process of reviewing your sources of income and budgeting for your expenses. It is important to consider both ongoing living expenses as well as future one-time expenses. A basic tenet of financial planning is to ensure you have an adequate emergency fund of 3-6 months’ worth of expenses in easily accessible cash not exposed to market risk. Plans should review lines of credit and debt management, including mortgages.

A thorough review of your tax return should be an integral part of a good financial plan. When you understand what tax bracket you are in currently and what bracket you are projected to be in in the future, you can make better decisions on tax planning strategies. This might include a Roth conversion, health savings and flexible spending accounts, and/or charitable giving. By incorporating investment management into tax planning, you can leverage tax-sensitive investing, reviewing cost basis and gains, utilizing tax loss harvesting, and tax loss carryforwards.

Once you have a good idea of where you currently stand and projections for how the plan will progress, it is important to ensure you have proper risk coverage. At a minimum, you should have health insurance so you can get the care you need and disability insurance in case you are unable to work. In the case of a catastrophic event, having adequate liability coverage can be the difference between making or breaking a financial plan. Not every insurance policy is the same, so you need to understand your coverage, deductible, and policy riders. If your family depends on your income to fund living expenses and you have large liabilities, such as a mortgage, it may be prudent to have a life insurance policy.

After working hard and savings for years, you may start to wonder when you can retire and sail off into the sunset. You may have some bucket list items or goals you would like to achieve. Cash flow analysis of your budget and retirement accounts can determine if you have enough assets to fund living expenses through retirement. Retirement often means a drop in income, which can present some tax planning opportunities. You will also need to decide when to start taking social security. You may have annuity or pension income. This will all affect strategies to optimize the withdrawals from your IRAs or 401ks or the possibility of a Roth conversion.

One of the most important (yet often overlooked) aspects of a financial plan is estate planning. Everyone should have a will and if you live in a state where probate is expensive and lengthy (like California), possibly a revocable living trust. You should address healthcare power of attorney and/or a living will. If you have young children, you can designate guardians. For those with sizeable estates, there are many strategies using Irrevocable Trusts or Irrevocable Life Insurance Trusts to reduce estate taxes, as 40% of your assets will go to the government over a certain threshold.

Finally, you may be interested in aiding loved ones. This may be in the form of gifts to Irrevocable Trusts for the benefit of your children or custodial accounts such as UTMAs or UGMAs. There are also tax-advantaged vehicles known as 529 plans to save for childrens’ college education expenses. There may be a need to care for elderly parents. In the event that a marriage does not work out, understanding the ramifications of splitting assets and income can have a huge effect on your financial future.

While every financial plan will look a little different as people have different areas of focus, there are some basic principles which must be addressed. A financial plan is a living, breathing document which will change as your life progresses. It provides a valuable roadmap to your future and enables you to make educated decisions on the path to financial security.

Individual investment positions detailed in this post should not be construed as a recommendation to purchase or sell the security. Past performance is not necessarily a guide to future performance. There are risks involved in investing, including possible loss of principal. This information is provided for informational purposes only and does not constitute a recommendation for any investment strategy, security or product described herein. Employees and/or owners of Nelson Capital Management, LLC may have a position securities mentioned in this post. Please contact us for a complete list of portfolio holdings. For additional information please contact us at 650-322-4000.

Receive our next post in your inbox.