Nelson Capital Management

Is Inflation on the Horizon?

May 20, 2021

Is Inflation on the Horizon?

In response to the pandemic, the U.S. government provided massive amounts of fiscal stimulus. Beginning with the CARES Act passed in 2020, and followed by the more recent $1.9 trillion American Rescue Plan Act of 2021, the total amount of stimulus passed in the last 12 months stands at about $5.3 trillion or nearly 25% of GDP. Attention has now turned toward yet another stimulus package (aimed at supporting infrastructure) that could be worth $3 trillion. Taken together, this wave of stimulus has sparked concerns that the U.S. could be on the path toward high inflation. As the economy opens back up and consumers are eager to spend, we could be facing a scenario where too many dollars are chasing too few goods and services. History has shown that inflation can have a significant impact on stocks and bonds, but predicting it is very difficult.

Fears of inflation have gone unrealized for years. Despite the large stimulus programs launched in response to the financial crisis in 2008-2009, over the last decade, the U.S. has seen slow economic growth and inflation below the Federal Reserve’s target level of 2%. Inflation has not been a real problem since the 1970s when easy monetary policy, energy shortages and government price controls led to double-digit inflation.

Is this time different?

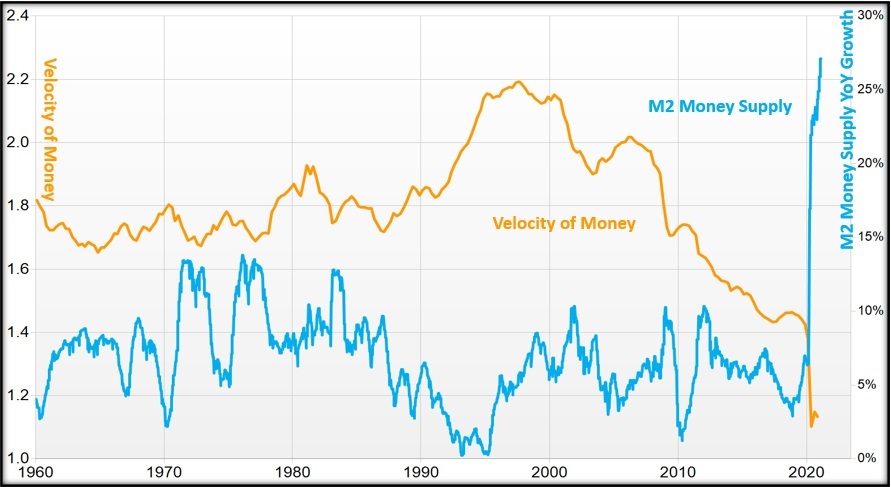

Since February 2020, the quantity of money in the U.S. economy, measured by M2 Money Supply, has increased by $4 trillion or 25%. This is the largest increase since the 1940s when the government was forced to print money to fund its WWII efforts.

Although money supply has increased, the velocity of money has dropped at almost an equally staggering rate. The velocity of money is defined as the rate at which money is exchanged in the economy. During inflationary periods, velocity generally rises as consumers spend more rapidly in anticipation that future prices will be higher, and today’s dollars will lose value tomorrow. In the decade since the financial crisis, the velocity of money has slowed as regulations have forced banks to hold more cash and consumers have been staying home and saving money.

Although money supply has increased, the velocity of money has dropped at almost an equally staggering rate. The velocity of money is defined as the rate at which money is exchanged in the economy. During inflationary periods, velocity generally rises as consumers spend more rapidly in anticipation that future prices will be higher, and today’s dollars will lose value tomorrow. In the decade since the financial crisis, the velocity of money has slowed as regulations have forced banks to hold more cash and consumers have been staying home and saving money.

An increase in money supply alone will not cause inflation. Money creation must stimulate lending and spending for prices to be pushed higher. We compared the current U.S. money supply increase to German money supply levels during the 1920s when the country experienced hyperinflation. We are orders of magnitude away from the increase in German money supply levels post-WWI.

We believe that the record drop in the velocity of money supports the view that surging money supply will not lead to rising prices in the short-term. Significant slack in the economy with high unemployment and advances in technology lead us to believe that it will take time before inflation picks up.

Individual investment positions detailed in this post should not be construed as a recommendation to purchase or sell the security. Past performance is not necessarily a guide to future performance. There are risks involved in investing, including possible loss of principal. This information is provided for informational purposes only and does not constitute a recommendation for any investment strategy, security or product described herein. Employees and/or owners of Nelson Capital Management, LLC may have a position securities mentioned in this post. Please contact us for a complete list of portfolio holdings. For additional information please contact us at 650-322-4000.

Receive our next post in your inbox.