Nelson Capital Management

In Lieu of RMDs, Consider Roth Conversion

Taxes, The Economy, Wealth Management

September 17, 2020

In Lieu of RMDs, Consider Roth Conversion

In the first quarter of this year, we wrote about the Coronavirus Aid, Relief, and Economic Security (CARES) Act of 2020. In that Act are provisions related to individual retirement accounts (IRAs). Some of these provisions allow relief for all indivduals, enabling access to assets in their IRA accounts, without penalty, to help those that might have seen their incomes impacted by COVID-19. The more meaningful provision for clients of Nelson Roberts is the waiving of the required minimum distribution (RMD) for calendar year 2020.

In the first quarter of this year, we wrote about the Coronavirus Aid, Relief, and Economic Security (CARES) Act of 2020. In that Act are provisions related to individual retirement accounts (IRAs). Some of these provisions allow relief for all indivduals, enabling access to assets in their IRA accounts, without penalty, to help those that might have seen their incomes impacted by COVID-19. The more meaningful provision for clients of Nelson Roberts is the waiving of the required minimum distribution (RMD) for calendar year 2020.

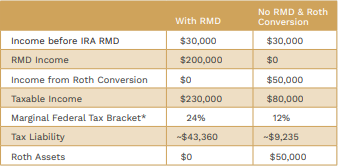

The following is a case study detailing how a client might utilize the suspension of the RMD requirement in 2020 to fund a Roth IRA account:

Scenario:

• Married couple in their 80s with Social Security income of $30,000.

• The couple has a required minimum distribution of $200,000 in 2020 from their IRAs.

• The couple has non-retirement assets of $1.5 million.

In a normal year, the combination of Social Security income and RMD would put them in a federal tax bracket of 24%. By electing not to take an RMD in 2020, this couple would only have Social Security income, which would put them in the 12% federal tax bracket.

In consultation with their tax accountant and Nelson Roberts relationship manager, this couple could determine how much of their IRA they could instead convert into a Roth IRA. The long-term benefit of a Roth IRA is that it grows tax free and is not subject to future income taxes for either the couple or potentially their Roth IRA beneficiaries upon withdrawal.

In the above scenario, the couple could convert approximately $50,000 of their current IRAs into a Roth IRA and remain in the 12% federal tax bracket. They would then pay federal taxes of $6,000 on the $50,000 conversion.

A conversion can be especially beneficial when the client couple has access to non-retirement assets to fund their living expenses and the tax liability created by the Roth conversion. It can also be valuable in a scenario where the ultimate beneficiaries of their Roth IRA, often the IRA owner’s children, are in high tax brackets.

Please contact your Nelson Roberts relationship manager to determine if a Roth IRA conversion might be of value to you.

Individual investment positions detailed in this post should not be construed as a recommendation to purchase or sell the security. Past performance is not necessarily a guide to future performance. There are risks involved in investing, including possible loss of principal. This information is provided for informational purposes only and does not constitute a recommendation for any investment strategy, security or product described herein. Employees and/or owners of Nelson Roberts Investment Advisors, LLC may have a position securities mentioned in this post. Please contact us for a complete list of portfolio holdings. For additional information please contact us at 650-322-4000.

Receive our next post in your inbox.