Nelson Capital Management

DocuSign Inc.

Asset Management, Companies and Industries, Investment Themes, The Economy

August 13, 2020

DocuSign Inc.

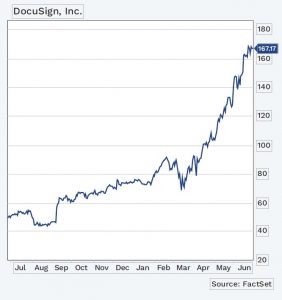

As the shelter-in-place orders started to go into effect around the country in March, many companies scrambled to configure effective remote work environments for their employees. We initiated a position in DocuSign (tkr: DOCU) at the beginning of the quarter, recognizing that the company would likely benefit from the new work-from-home trend. DocuSign is most well-known for its e-signature solution, which management estimates has a $25 billion total addressable market. DocuSign is the clear leader in the space, by at least a factor of two. There is potential for the company to increase their revenue opportunity as they add ancillary features. DocuSign has been effective at this “land and expand” strategy, as customers continue to add on additional products and services. Even as employees begin returning to work, companies are unlikely to stop using DocuSign, as they realize the time savings and cost effectiveness of electronic document execution.

One of DocuSign’s key offerings is Agreement Cloud. This software suite helps automate the entire agreement process. Agreement Cloud consists of DocuSign’s core eSignature solution as well as other applications for automating pre- and postsignature processes. These include automatically generating an agreement from data in other systems, supporting negotiation workflow, collecting payment after signatures, and using AI to analyze a collection of agreements for risks and opportunities.

Relative to other software companies, DocuSign’s market is remarkably less saturated. It sells into a broad range of customer verticals: financial services, insurance, real estate, mortgage, government, education, healthcare, life sciences, etc. Government is a significant and upcoming opportunity. The Department of Labor recently adopted DocuSign to help streamline its process for handling emergency unemployment benefits alongside the colossal wave of claims filed since the middle of March. DocuSign went public in May 2018, although the company was founded in 2003. The U.S. government passed the Uniform Electronic Transactions Act and the Electronic Signatures in Global and National Commerce Act in 1999 and 2000, respectively. These laws helped legitimize electronic signatures, but the trend has really taken off in the last 10 years. Early e-signature tools were clunky and complex, and DocuSign has been successful in capturing the market by offering a simple, streamlined solution that has gained significant brand recognition over time.

Relative to other software companies, DocuSign’s market is remarkably less saturated. It sells into a broad range of customer verticals: financial services, insurance, real estate, mortgage, government, education, healthcare, life sciences, etc. Government is a significant and upcoming opportunity. The Department of Labor recently adopted DocuSign to help streamline its process for handling emergency unemployment benefits alongside the colossal wave of claims filed since the middle of March. DocuSign went public in May 2018, although the company was founded in 2003. The U.S. government passed the Uniform Electronic Transactions Act and the Electronic Signatures in Global and National Commerce Act in 1999 and 2000, respectively. These laws helped legitimize electronic signatures, but the trend has really taken off in the last 10 years. Early e-signature tools were clunky and complex, and DocuSign has been successful in capturing the market by offering a simple, streamlined solution that has gained significant brand recognition over time.

DocuSign’s segments are Subscription (94% of revenue) and Professional Services (6% of revenue). A high percentage of its revenue recurs, based on contracts of 12-18 months. The stock has run up significantly since we bought it, and its valuation is now arguably expensive. However, we believe DocuSign’s success is likely to continue because of the overall improved efficiency and the cost savings it brings to companies, even as we return to “normal” times.

Individual investment positions detailed in this post should not be construed as a recommendation to purchase or sell the security. Past performance is not necessarily a guide to future performance. There are risks involved in investing, including possible loss of principal. This information is provided for informational purposes only and does not constitute a recommendation for any investment strategy, security or product described herein. Employees and/or owners of Nelson Roberts Investment Advisors, LLC may have a position securities mentioned in this post. Please contact us for a complete list of portfolio holdings. For additional information please contact us at 650-322-4000.

Receive our next post in your inbox.