Nelson Capital Management

Expansion Outlook Extends

Asset Management, Investment Themes, The Economy

July 9, 2019

Expansion Outlook Extends

The generally positive market trends that began in January of this year continued into the second quarter. The S&P 500 reached a new high of 2,945 on April 30th, surpassing last September’s record. In May, equities took a turn lower as President Trump ramped up trade threats against both China and Mexico. The tariffs threatened against Mexico were immigration-related, an unusual tactic that some Republican lawmakers did not support. One of our clients astutely pointed out that Trump “uses tariffs the way Teddy Roosevelt used battleships.” In any case, the U.S. and Mexico eventually reached a deal on immigration and the threat of tariffs on Mexican goods was removed— for now—allowing the S&P to recover from the downturn, reaching yet another all-time high and finishing the quarter at 2,942.

The last three labor reports revealed overall healthy job growth, allaying any concerns about a slowdown in the job market after February’s disappointing 20,000 nonfarm payrolls number. However, the reports also showed signs of plateauing wage growth, with average hourly earnings growth decelerating to 3.1% from 3.4% at the beginning of the year. Inflation data has also indicated softness, both in the Consumer Price Index (CPI) data and in the Personal Consumption Expenditure (PCE) data, the latter being the measure the Federal Reserve watches more closely. The upward inflationary pressure of a tight labor market seems to be losing the battle against downward inflation pressures. Low inflation abroad, depressed commodity prices, concerns about an overall slowdown in China and ongoing trade jitters continue to keep a lid on U.S. inflation. Even real estate prices have leveled off and we are seeing signs of depressed shipping prices. This anemic inflation, along with more recent trade disruptions, has turned discussion of a Federal Reserve “pause” in its rate hike program earlier this year into an outright expectation of interest rate cuts in 2019. Although the Fed resisted pressure to cut rates at its June meeting, several policymakers expressed that they are open to cutting rates in the coming months.

The last three labor reports revealed overall healthy job growth, allaying any concerns about a slowdown in the job market after February’s disappointing 20,000 nonfarm payrolls number. However, the reports also showed signs of plateauing wage growth, with average hourly earnings growth decelerating to 3.1% from 3.4% at the beginning of the year. Inflation data has also indicated softness, both in the Consumer Price Index (CPI) data and in the Personal Consumption Expenditure (PCE) data, the latter being the measure the Federal Reserve watches more closely. The upward inflationary pressure of a tight labor market seems to be losing the battle against downward inflation pressures. Low inflation abroad, depressed commodity prices, concerns about an overall slowdown in China and ongoing trade jitters continue to keep a lid on U.S. inflation. Even real estate prices have leveled off and we are seeing signs of depressed shipping prices. This anemic inflation, along with more recent trade disruptions, has turned discussion of a Federal Reserve “pause” in its rate hike program earlier this year into an outright expectation of interest rate cuts in 2019. Although the Fed resisted pressure to cut rates at its June meeting, several policymakers expressed that they are open to cutting rates in the coming months.

This dramatic shift in the Fed’s stance has helped drive the equity markets back up to summer 2018 levels. Despite the fact that the S&P 500 is up 18% this year, stocks are not overvalued. At a price-to-earnings (P/E) ratio of about 16.5 times forward earnings, the S&P 500 is right in line with its 25-year average valuation. 2019 has seen an impressive lineup of companies launch their initial public offerings (IPOs), with mixed overall results thus far. Many of these IPOs are former “unicorns,” or companies that carried valuations higher than $1 billion in the private market. Pinterest (tkr: PINS) and Zoom (tkr: ZM) have taken off since their public debuts while rideshare companies Uber (tkr: UBER) and Lyft (tkr: LYFT) have struggled to surpass their IPO prices.

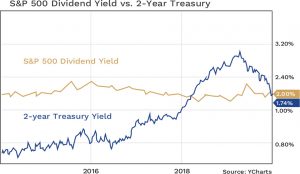

It feels like there is a general apathy toward stocks, which likely suggests that we will not see much in the way of a price-to-earnings multiple expansion this year. The margin boost from the tax cut last year has played out, and most companies expect a pause in earnings growth in 2019. For these reasons, we think returns on stocks will be driven by dividends and buybacks, and we continue to look to invest in companies that are focused on returning value to shareholders this way. Meanwhile, alongside the Fed’s pivot toward rate cuts, the 10-year Treasury yield has fallen precipitously, from over 3% last fall to 2.00%. In fact, the entire yield curve dropped, and the 2-year Treasury no longer offers a yield that is higher than the S&P’s dividend yield, as it had for the past year.

It feels like there is a general apathy toward stocks, which likely suggests that we will not see much in the way of a price-to-earnings multiple expansion this year. The margin boost from the tax cut last year has played out, and most companies expect a pause in earnings growth in 2019. For these reasons, we think returns on stocks will be driven by dividends and buybacks, and we continue to look to invest in companies that are focused on returning value to shareholders this way. Meanwhile, alongside the Fed’s pivot toward rate cuts, the 10-year Treasury yield has fallen precipitously, from over 3% last fall to 2.00%. In fact, the entire yield curve dropped, and the 2-year Treasury no longer offers a yield that is higher than the S&P’s dividend yield, as it had for the past year.

The current economic expansion has now officially become the longest on record. Nevertheless, we see no signs of imminent collapse, despite near-term market volatility over trade tensions. The two primary indicators we are monitoring do not point to a recession any time soon: year-over-year U.S. job growth is still well over 1% and the spread between the 2- and 10-year Treasury yields is still positive, and in fact has widened in recent weeks to about 0.30% from about 0.14% at the end of May. We have a long way to go until the 2020 election, and the inevitable food fight among Democratic candidates will no doubt provide plenty of sensational soundbites in the meantime, but this should only result in near-term headline risk until a candidate is chosen next year. We remain fully invested and focused on our pivot toward more defensive, value-oriented stocks that offer dividend income as opposed to growth companies that are more dependent on capital gains.

Individual investment positions detailed in this post should not be construed as a recommendation to purchase or sell the security. Past performance is not necessarily a guide to future performance. There are risks involved in investing, including possible loss of principal. This information is provided for informational purposes only and does not constitute a recommendation for any investment strategy, security or product described herein. Employees and/or owners of Nelson Roberts Investment Advisors, LLC may have a position securities mentioned in this post. Please contact us for a complete list of portfolio holdings. For additional information please contact us at 650-322-4000.

Receive our next post in your inbox.