Nelson Capital Management

Market Bounces Back

Asset Management, Companies and Industries, Investment Themes, The Economy

April 9, 2019

Market Bounces Back

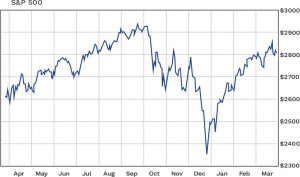

The clouds of uncertainty that dragged equity markets down in the fourth quarter began to part at the beginning of 2019. Between October 1 and Christmas Eve, the S&P 500 fell 19.2%, narrowly missing the 20% threshold that would qualify the downturn as a bear market. However, starting December 26, market sentiment generally began to turn cautiously optimistic as retailers such as Amazon reported a record-breaking holiday season.

On January 4, the December jobs report provided more good news, revealing that a whopping 312,000 jobs were added during the month, while the prior month’s number was revised higher. More uncertainty was removed when the government shutdown that began three days before Christmas finally came to an end on January 25. The tough trade talk that had brewed skepticism over the ongoing trade war began to turn more positive, as officials expressed optimism that the U.S. and China might actually reach a deal. On February 24, President Trump announced that the tariff increases that had been planned for March 1 would be delayed, citing progress in trade negotiations.

On January 4, the December jobs report provided more good news, revealing that a whopping 312,000 jobs were added during the month, while the prior month’s number was revised higher. More uncertainty was removed when the government shutdown that began three days before Christmas finally came to an end on January 25. The tough trade talk that had brewed skepticism over the ongoing trade war began to turn more positive, as officials expressed optimism that the U.S. and China might actually reach a deal. On February 24, President Trump announced that the tariff increases that had been planned for March 1 would be delayed, citing progress in trade negotiations.

The equity markets continued to march higher as companies began reporting earnings that were generally better than expected. Overall, fourth quarter S&P 500 company earnings rose 12%, capping off a full year of stellar earnings growth fueled by the Tax Cut and Jobs Act.

Meanwhile, the Federal Reserve telegraphed that it would take a pause in its rate hike program this year following the four increases to its target rate in 2018. Against a backdrop of tame inflation, low commodity prices and global growth concerns, the Fed reiterated that it plans to remain patient and take a “wait-and-see” approach to any future rate increases.

By the end of the first quarter, the equity markets had nearly recovered from the sharp correction at the end of last year. The S&P 500 rose 13.6%, bringing it to 2,895, just shy of the September 20th all-time high of 2,930. The volatility that was a hallmark of the fourth quarter of 2018 has been largely absent thus far in 2019.

By the end of the first quarter, the equity markets had nearly recovered from the sharp correction at the end of last year. The S&P 500 rose 13.6%, bringing it to 2,895, just shy of the September 20th all-time high of 2,930. The volatility that was a hallmark of the fourth quarter of 2018 has been largely absent thus far in 2019.

Internationally, growth remains challenged. The International Monetary Fund revised down its estimates for global growth, the second downward revision in three months. The undeniable slowdown in the Chinese economy, coupled with the yet-to-be-resolved trade war between the U.S. and China, was part of the reasoning behind the downward revision. Furthermore, the confusion surrounding how the Brexit will actually occur and what the impact will be remains a question mark that complicates global growth estimates. Nearly three years after the British people voted to exit the European Union, no official plan has been agreed upon. The European Central Bank, which had three months ago decided to end its stimulative bond-buying program, reversed course and began adding stimulus measures back in following cuts to its forecasts for euro-area growth and inflation.

At home, the U.S. labor market continued its powerful streak. In December and January, the U.S. added an average of ~270,000 per month. However, the most recent report showed that the labor market only added 20,000 jobs in February, far below the estimated 180,000 jobs economists were expecting. We continue to track the year-over-year job growth rate, which tends to fall below 1% ahead of major recessions. But one mediocre jobs report is not a reason for heightened concern. The rapid pace of job increases over the last several months means that we likely do not have to worry about year-over-year job growth falling below 1% until the end of this year at the earliest. In this tight labor market, wages also continued their steady march higher, with average hourly earnings rising 3.4%.

In spite of rising wages and increasing labor costs, inflation remains elusive. Low commodity prices, stubbornly low rates abroad, economic weakness internationally, and a strong dollar appear to be outweighing the inflationary impact of the rising cost of labor. The German 10-year bond yield recently turned negative, and is currently 270 bps less than the U.S. 10-year Treasury yield. The U.S. Treasury yield curve remains technically inverted, with the 10-year bond yielding less than the 3-month note, although the more recognizable 2-year/10-year spread is still positive, hovering around 15 basis points, which is where it has been since early December. We continue to monitor the 2-year/10-year spread, as this tends to turn negative about 6 to 30 months ahead of a recession.

Recently, we began pivoting toward defensive stocks that should hold up well in a recession. We continue to be thoughtful about our equity selection, recognizing that we are in the later stages of the current economic cycle. If we see a resolution to the trade war with China and if the Federal Reserve remains committed to keeping rates low, we think the bull market may get a second wind. We do not recommend trying to time the market, but we are advising a thoughtful assessment of equity market exposure. The recovery from the fourth quarter dip provides an opportunity for us to reassess individual client asset allocations.

Individual investment positions detailed in this post should not be construed as a recommendation to purchase or sell the security. Past performance is not necessarily a guide to future performance. There are risks involved in investing, including possible loss of principal. This information is provided for informational purposes only and does not constitute a recommendation for any investment strategy, security or product described herein. Employees and/or owners of Nelson Roberts Investment Advisors, LLC may have a position securities mentioned in this post. Please contact us for a complete list of portfolio holdings. For additional information please contact us at 650-322-4000.

Receive our next post in your inbox.